Alu-Alu Blister Foil: Bangladesh's Overlooked Industrial Bottleneck

While our pharmaceutical industry thrives, domestic Alu-Alu blister production struggles to survive due to policy gaps — threatening jobs, investment, and supply chain resilience.

Bangladesh's pharmaceutical industry stands as one of the country's most remarkable industrial achievements. It currently meets approximately 98 percent of domestic demand and exports medicines to more than 150 countries across highly regulated markets in Europe and North America. Over the last five years, the sector has recorded cumulative growth of 12.1 percent. Industry insiders forecast an average annual growth rate of 15–16 percent over the next five years.

Yet behind this success lies a structural vulnerability that demands urgent policy attention: heavy dependence on imported Alu-Alu (cold-form) blister foil.

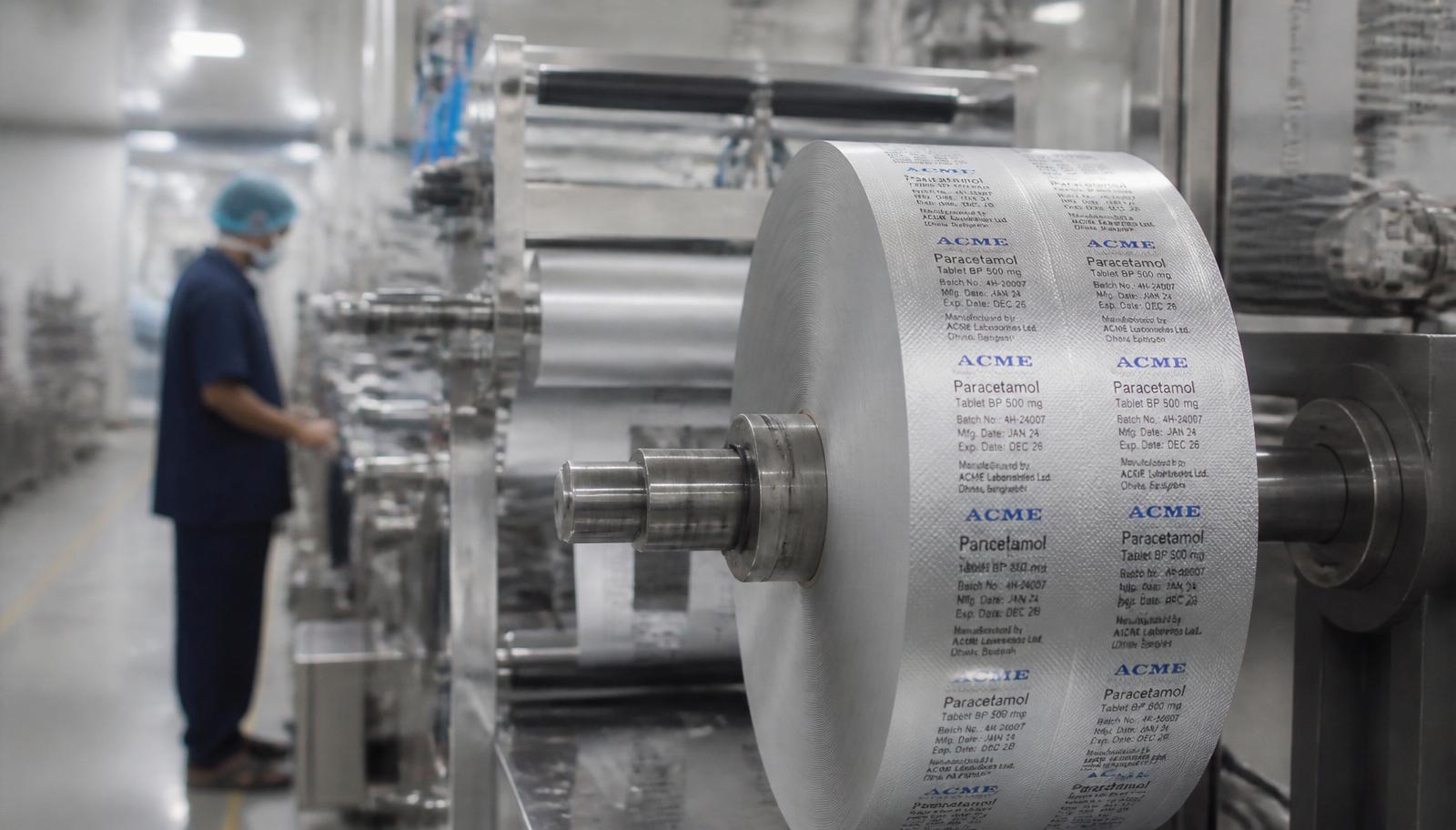

Alu-Alu blister foil is a high-barrier packaging material essential for moisture-sensitive and export-grade medicines. It provides superior protection against humidity, oxygen, and light — a critical feature in tropical climates like Bangladesh and in stringent regulatory markets. As pharmaceutical production expands and quality standards tighten, demand for high-barrier packaging inevitably rises.

The import-domination problem.

According to data collected from the National Board of Revenue (NBR), Bangladesh currently imports approximately 400–420 tons of Alu-Alu blister foil per month, while domestic production accounts for only 120–150 tons monthly. This places total national consumption at roughly 550–600 tons per month, equivalent to around 7,000 tons annually. Imports therefore dominate the market.

Over the past decade, nine companies invested in establishing Alu-Alu blister foil manufacturing facilities in Bangladesh. These investments were capital-intensive, requiring cold-forming technology, coating and lamination lines, testing laboratories, and skilled workforce development. However, the sector now faces serious survival risks.

Several firms have already exited. Today, only four companies remain operational, all running significantly below installed capacity. Persistent underutilisation has increased per-unit production costs and weakened financial sustainability. If this trend continues, further closures may follow — not due to lack of demand, but due to structural policy distortions.

Where demand is heading.

Although pharmaceutical growth over the last five years was 12.1 percent, forward-looking industry forecasts suggest 15–16 percent annual expansion. Even at a conservative 10 percent annual growth in Alu-Alu blister demand — below projected pharmaceutical growth — national requirement would evolve as follows (based on a 7,000-ton annual baseline):

Within five years, annual demand could exceed 11,000 tons. This indicates substantial market potential for domestic producers — if structural constraints are addressed.

The core competitiveness challenges.

First, tariff alignment does not adequately incentivise local value addition. When import duties on finished Alu-Alu products remain comparable to duties on raw materials used for domestic production, local manufacturers struggle to compete on price. Meanwhile, suppliers from India, China, and Korea operate within large-scale integrated ecosystems that significantly reduce their cost structures.

Second, domestic producers are required to pay Advance Income Tax (AIT) at two separate stages — during raw material import and again at the point of sale. In many cases, the cumulative AIT paid significantly exceeds the company's actual income tax liability. Although the framework technically permits adjustment or refund of excess payments, in practice recovery is rarely straightforward. Applications for adjustment often trigger prolonged review processes, including re-examination of declared sales and revenue figures. Differences in interpretation or assessment frequently result in refund claims being reduced, delayed, or effectively neutralised. Over time, companies find that the excess AIT paid does not return as working capital but remains trapped within the system. This persistent liquidity constraint ultimately transforms what is intended as an adjustable tax into a structural cost burden.

Third, prolonged underutilisation of installed capacity has created financial strain. When factories operate far below optimal levels, fixed costs are distributed over smaller volumes, pushing per-unit costs higher. This structural inefficiency discourages reinvestment and weakens long-term sustainability.

Strategic implications.

The implications extend beyond individual companies. Continued import dominance increases exposure to currency volatility, shipping disruptions, and geopolitical uncertainties. For a country whose pharmaceutical sector is a key export earner, reliance on imported critical packaging materials presents strategic vulnerability.

Strengthening domestic Alu-Alu production would create measurable benefits. Pharmaceutical companies would enjoy reduced lead times, improved supply reliability, and lower inventory holding requirements. Smaller consignment needs would ease storage pressure. Foreign currency outflow would decline. Skilled employment and industrial investment would be preserved.

Importantly, the sector remains recoverable. The four operational companies still possess installed machinery, trained manpower, and technical expertise. The five inactive firms represent dormant industrial assets that could potentially be revived under supportive conditions.

"The issue is not technological capability or capacity; it is policy alignment. Bangladesh already has the factories, technology, and skilled workforce required to meet a much larger share of domestic demand."

What is required is calibrated policy support — rationalised tariff differentiation, reform of the AIT mechanism to reduce working capital distortion, and an industrial framework that prioritises domestic value creation.

As Bangladesh moves toward LDC graduation and increased global competition, strengthening backward linkage industries will be essential for economic resilience. The future of the domestic Alu-Alu blister foil sector will depend not on demand — which is clearly expanding — but on whether policy reforms can ensure its survival and growth.